Tax Changes Under the Big Beautiful Bill

Tax Changes Under the Big Beautiful Bill

The One Big Beautiful Bill Act (OBBBA), also called the Big Beautiful Bill, was signed into effect on July 4, 2024. This sweeping legislation reshapes the federal tax rules with provisions directly affecting small business owners, nonprofits and real-estate entrepreneurs.

For many, the most important takeaway is that the bill locks in many of the 2017 tax cuts, making them permanent. It also introduces new deductions and credits that boost take-home income and incentivize some types of investment. At the same time, the legislation also reshuffles long-standing rules around deductions, family benefits and pass-through income. Understanding the Big Beautiful Bill tax implications is essential, especially for small business owners planning 2025 to 2028 budgets.

One Big Beautiful Bill Summary

Passed by Congress and signed into law in 2025, OBBBA, also codified as Public Law No. 199-21, covers hundreds of provisions across tax policy, health care, education and defense. The bill delivers a large package — approximately $4.5 trillion in tax cuts and $1.1 trillion in net spending cuts, resulting in around $3.4 trillion added to the deficit over the next decade. New and expanded deductions include:

- Eliminating taxes on tips and overtime up to specific caps.

- New auto loan interest deduction for U.S.-assembled vehicles.

- Elevated child tax credit and special deduction for older adults.

- Stricter work requirements and reduced provider taxes for Medicaid and the Supplemental Nutrition Assistance Program (SNAP).

- Expanding rural hospital funding and phasing out clean-energy tax incentives while promoting fossil fuel development.

- Phasing out existing student loan programs while creating new tax-advantaged “Trump Accounts.”

- Launching the Pell Grant expansion to support short-term workforce training programs starting in July 2026.

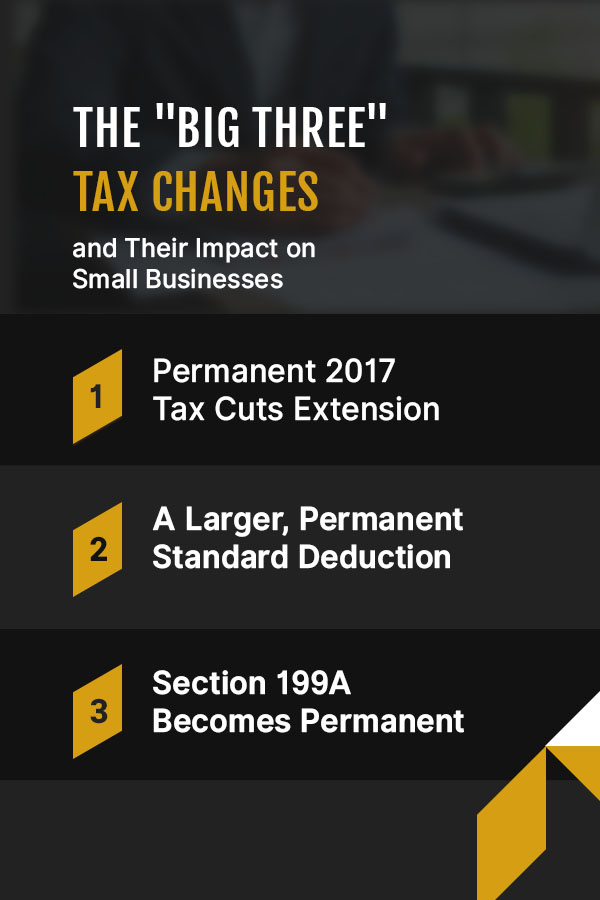

The “Big Three” Tax Changes and Their Impact on Small Businesses

If you own or manage a small business, this bill affects you. It influences your bottom line, payroll planning, investment strategies, and retirement or family savings. The changes are complex, but the essence is clear — the tax landscape has shifted, and now it’s time to understand what’s new.

1. Permanent 2017 Tax Cuts Extension

The Big Beautiful Bill is wide-ranging, but several provisions stand out for small business owners and nonprofit organizations. It makes the 2017 Tax Cuts and Jobs Act (TCJA) permanent. Before this, the lower income tax brackets and doubled standard deduction were set to expire in 2025 — but now they are here to stay.

This bill gives stability to business owners filing as pass-through entities, such as sole proprietorships, partnerships or S corporations. Predictable tax brackets make it easier to plan long-term investments, whether you’re buying new construction equipment, hiring staff or assembling a property portfolio.

2. A Larger, Permanent Standard Deduction

The standard deduction nearly doubled under the 2017 tax law, and the Big Beautiful Bill makes that increase permanent and boosts it further through 2028. For 2025, the deduction is $25,000 for joint filers and $12,500 for individuals. Older adults over age 65 have an additional $6,000 deduction through 2028. If an individual’s income is over $75,000, the deduction phases out.

These deductions matter for small business owners who may not have enough itemized deductions to exceed the standard threshold. For example, a business running a small shop may find that the standard deduction simplifies filing while still delivering significant tax relief.

3. Section 199A Becomes Permanent

The permanent 20% pass-through deduction on qualified business income (QBI) is another win for entrepreneurs. This deduction was originally introduced in 2017 and allows small businesses to deduct up to 20% of their qualified income before calculating taxable income. The Big Beautiful Bill extends this permanently and expands the income thresholds, meaning more businesses qualify.

For instance, a real-estate investor earning $200,000 in qualified business income can deduct $40,000 before paying federal tax. That’s money you can reinvest in property improvements, staffing or reserves.

Additional Provisions Affecting Small Businesses

Beyond the big three, several new and revised provisions are adding meaningful benefits for small business owners:

- State and Local Tax (SALT) deduction relief: The deduction cap temporarily rises from $10,000 to $40,000 for 2025 and increases 1% annually through 2029, giving those in high-tax states relief. For example, a nonprofit property manager in New Jersey can now deduct far more in state taxes, reducing federal liability.

- Permanent bonus depreciation: Small firms can keep fully expensing qualifying equipment and software purchases immediately rather than depreciating over years.

- Child Tax Credit Expansion: The credit increases to $2,000 per child, adjusted annually for inflation. For entrepreneurs with families, this represents straightforward cash-flow relief.

- Tax-free tips and overtime: Workers earning tips or overtime can exclude a portion from taxable income, a major benefit for nonprofits employing tipped staff or contractors with variable days.

- Auto-loan interest deduction: Interest on certain auto loans becomes deductible, an advantage for construction firms financing work vehicles.

- Trump Accounts: Parents of children born between 2025 and 2028 can open these special accounts, which allow tax-deferred savings for education or future expenses. For small business owners, these accounts can double as a retirement and succession-planning tool.

- Streamlined reporting requirements: The revised IRS guidance reduces certain paperwork burdens but imposes stricter verification for wage and tip reporting.

- Targeted workforce credits: Temporary credits will encourage hiring and training in specified industries through 2028.

Eligibility depends on your business income thresholds, the type of entity and compliance with new reporting rules. Pass-through businesses and self-employed workers benefit most but must track phase-outs carefully. While lower tax brackets and higher standard deduction are permanent, several new deductions, such as tips, overtime and car loans, expire after 2028 unless Congress renews them. Rising deficits and election cycles can also trigger amendments or new surtaxes in the future, making it essential to partner with a tax professional who stays apprised of any changes to tax bills that may affect you or your business.

The Pros and Cons of OBBBA Changes

The Big Beautiful Bill does not end TCJA — instead, it locks in many provisions and adds new deductions. These changes bring clear advantages but also introduce costs and complexities. Here’s a snapshot of the key pros and cons you should weigh:

| Pros | Cons |

| Permanent tax certainty. Default tax cuts and standard deductions stay in effect beyond 2025. | High cost. Extending TCJA provisions adds trillions to deficits. CBO estimates around $4 to $4.6 trillion over 10 years. |

| Expanded deductions for working Americans. Tips, overtime and auto loan interest become newly deductible, potentially boosting take-home pay. | Potential complexity. New deductions come with phase-outs, SSN requirements and stricter employee reporting. |

| Enhanced support for families and older adults. Higher child tax credit and a temporary older adult extra deduction reduce liabilities. | There are sunsets ahead. Some enhancements expire after 2028. |

| Business investment incentives continue. Permanent bonus depreciation and research and development expensing encourage growth. | Energy policy reversals. OBBBA phases out renewable tax credits, potentially hindering clean energy development. |

| Alignment with global tax standards. Corporate international taxation reforms reduce profit shifting. | Equity and stability concerns. Higher deficits may raise inflation, debt servicing costs and widening inequality. |

What Does This Mean for Individual Tax Filing?

The Big Beautiful Bill gives small business owners certainty by locking in lower rates originally created under TCJA. It also simplifies and expands opportunities:

- Simplified filing: With the larger standard deduction, fewer taxpayers need to itemize. A nonprofit director who used to track mortgage interest and charitable deductions may now use the standard deduction, which delivers more savings with less paperwork.

- Family benefits: The higher child tax credit puts more money back in parents’ pockets. For example, parents with children under 17 can get up to $6,600 in credits.

- Older adult support: Retirees and older business owners benefit from the extra senior deduction of $6,000, making it easier to stretch retirement income.

This impact on individual tax filing means that, for example, a contractor with two kids, $80,000 in income and standard deductions can see their taxable income drop by $30,000 after deductions and credits. A retired landlord aged 67 can claim the extra senior deduction, lowering their liability and preserving rental income for living expenses.

Does Filing Change Under OBBBA?

Filing is still fundamentally similar. You still use Form 1040 with standard schedules — not an overhaul of the filing process. However, your tax return looks different. You may see new lines or fields for the new deductions, stricter documentation requirements and more calculations because of the phase-outs for Modified Adjusted Gross Income (MAGI)-based eligibility. As a taxpayer, you need to track income thresholds and deduction limits.

Navigating State and Local Tax Implications

The changes to SALT deductions deserve special attention. The higher $40,000 cap is significant in high-tax states like California and New York. Real-estate professionals often pay steep property taxes, and this provision lets them deduct more of those costs. The SALT deduction has less impact for business owners in low-tax states like Texas or Florida, but the standard deduction and pass-through benefits still offer meaningful relief.

Nonprofit organizations with large property holdings or offices in urban centers may see lower taxable income through higher SALT deductions, improving cash flow for mission-based work.

How to Prepare

OBBBA is one of the most sweeping legislative packages of 2025. It locks in and deepens tax cuts for many, introduces new deductions and financial tools, while rolling back parts of the social safety net and reshaping health care, education and energy policy. Its depth and breadth make strategic financial planning more critical than ever. The Big Beautiful Bill creates opportunities, but realizing those benefits depends on your planning. Here are the steps to take:

- Review your filing strategy: Work with your tax advisor to decide whether to itemize or claim the larger standard deduction. You may find the standard deduction more advantageous.

- Maximize the pass-through deduction: Check whether your business income qualifies under Section 199A, which may involve restructuring, adjusting payroll or re-evaluating contracts.

- Track tips and overtime carefully: For hospitality, construction or nonprofit businesses employing tipped workers, set up systems to record exempt income accurately.

- Plan for state taxes: If you operate in a high-tax state, take advantage of the higher SALT cap while it lasts.

- Consider Trump Accounts: For families with children, see if these accounts align with your education and savings goals.

- Stay flexible: Not all provisions are permanent. Build strategies that allow for adjustment if deductions sunset or thresholds shift.

Note Key Dates

Be sure you understand OBBBA’s key milestones and deadlines. Aligning business purchases, payroll timing, and family planning with these milestones can maximize the law’s benefits:

- January 1, 2025: At the start of 2025, the TCJA tax brackets, standard deductions and pass-through deductions become permanent.

- January 1, 2025, to December 31, 2028: The temporary enhanced child tax credit, a tip income deduction, overtime pay deduction and auto loan interest deduction are in effect for three years.

- April 15, 2026: April 2026 is the deadline to file 2025 tax returns under the Big Beautiful Bill’s new deductions.

- 2027 to 2028: Phase-outs and inflation adjustment continue annually, and the IRS will release updated guidance each fall.

Working with seasoned tax planning and compliance professionals means you have someone reliable to interpret new tax rules and adjustments, ensuring you claim all benefits properly. They manage phase-outs deliberately, helping you avoid costly errors, and they stay current with IRS guidance to keep you compliant. Professionals can also help your business plan purchase timing so you can benefit from bonus depreciation, structure car purchase financing to maximize the new auto-loan interest deduction, and identify if your business qualifies for small-business pass-through enhancement and R&D expensing.

Get Guidance on Tax Changes With Marshall Jones

OBBBA cements key tax benefits while introducing new deductions that can reshape planning for many of us. With the TCJA expiration approaching, OBBBA stepped in to preserve key deductions and credits for individuals and small businesses. However, some new act adjustments are temporary. Unless extended again, related changes, such as higher SALT deductions, will revert after 2028. Your business should plan with this in mind — better yet, partner with a reliable financial professional to help you navigate current and future tax changes.

For over 30 years, the professionals at Marshall Jones have been working with businesses through certified public accountants and advisors. Our CPA accounting services include audits, reviews, compilations, tax compliance, research, year-end financial statement audits and outsourced accounting services. With us, you enjoy customized accounting, time savings, lower costs and professional accounting services that give you peace of mind, knowing you’re tax-compliant.

Contact us today for more information or to sign up and make the most of the OBBBA changes.