How Can Accurate Financial Reporting Help Secure Grants for Nonprofits?

Grants are often governed by strict regulatory frameworks, especially those that come from government agencies. State and private grantors also have their own compliance standards and agreement terms. These requirements ensure that nonprofits use grant funds appropriately and effectively. Some grantors offer grants in the form of reimbursements to prevent fund misuse.

Regardless of the grant terms, keeping accurate financial reports improves your relationship with the grantor. Your transparency and accountability improve trust and impact your nonprofit’s reputation. Different grant types come with different reporting expectations. Marshall Jones explains how accurate financial reporting increases your chances of grant approval.

Key Takeaways

Accurate financial reporting increases your chances of securing grants because it helps you:

- Comply with relevant regulations.

- Manage expenses according to grant terms.

- Present past achievements through tangible and measurable results.

- Showcase your trustworthiness and avoid penalties or accusations of fraud.

Why Is Accurate Financial Reporting Crucial for Nonprofits Seeking Grants?

Accurate financial reporting strengthens your relationships with grantors, auditors and other stakeholders. Here’s how it can help you secure future grants:

1. Meets Regulations and Reporting Obligations Set by Grantors

Grants must follow relevant federal and state regulations, especially if they’re provided by government institutions. The Federal Funding Accountability and Transparency Act established the government-wide reporting procedure that requires organizations receiving federal funds to publicly disclose their information. Among other requirements, you need to provide your organization’s name, grant amount, funding agency and location. You also need to report the following:

- Financial data: The expenses you paid for using federal funds

- Compliance information: Information that showcases your compliance with federal regulations

- Project data: Your progress report or community impact

Relevant agencies may collect this information through regular progress reports, site visits and audits.

Specific grant requirements will be found in the Notice of Award. With government grants, you’re required to submit a Federal Financial Report annually, unless you’re receiving domestic awards under the Streamlined Noncompeting Award Process or otherwise stated. When required annually, you may need to submit the report for each budget period up to 90 days after the end of the calendar quarter.

Grants can come with other requirements, and their stringency depends on the grant type. Restricted grants can only be used for specific purposes as determined by the grantor, while unrestricted grants can often be used at your nonprofit’s discretion. Whichever grant you have, accurate financial reporting maintains transparency and demonstrates compliance with terms and regulations.

2. Assigns Costs to the Appropriate Grants, Programs and Operational Categories

Properly allocating expenses avoids overspending and fund misuse. Having a paper trail with clear, traceable financial records also makes reporting less stressful when deadlines approach. Maintaining thorough documentation involves keeping receipts, invoices, timesheets and other records that support audits. This data proves your reliability in complying with grant terms.

Additionally, grant funds often need to be separated from other funds when tracking spending. You can use unique fund codes when monitoring spending to understand which expenses tie to which grant. This level of granularity improves the accuracy of your statements. It also reflects your nonprofit’s financial position, supporting board decisions and public disclosures.

3. Presents How Funding Contributed to the Organization’s Achievements

Alongside financial statements, grants may require performance reports, which involve a combination of quantitative and qualitative data. This performance report demonstrates how the funds have contributed to your projects and whether your activities have benefited the community or the environment. It helps create a well-articulated mission statement that captures your nonprofit’s purpose and strategic direction. You should also define specific project outcomes you wish to achieve and their respective indicators.

For instance, the National Institutes of Health (NIH) requires grant recipients to submit a research performance progress report annually as part of the noncompeting continuation award process. Among other requirements, the reports should incorporate:

- The organization’s accomplishments.

- Plans for the next year.

- Produced manuscripts and publications.

- Involved project personnel.

- Project challenges, delays and plans to resolve them.

Accurate financial and progress reports highlight past achievements and build credibility and stakeholder trust. They tell potential grantors that your nonprofit has made a tangible difference. For instance, you can highlight the number of beneficiaries you’ve served or the number of graduates in your program. Combining qualitative stories with quantitative data enables you to create a strong case for your nonprofit’s mission.

4. Avoids Penalties and Funding Loss

Grant funding is susceptible to fraud, waste and abuse. Inaccurate financial reports raise suspicion about whether you’re using the funds based on the agreement. Using grant funds for personal gain, unjust enrichment or other purposes than their intended use is a form of theft. People involved could be subject to criminal and civil prosecution, where violations can include:

- False claims

- False statements

- Theft or bribery

- Embezzlement

- Mail fraud and wire fraud

Accurate financial reports protect your nonprofit and enable you to spot fraud immediately. Regularly reviewing spending, timelines and compliance with grant terms can help you avoid clawbacks, where grantors take back the funds they’ve provided due to noncompliance. These clawbacks are possible for grants with clauses that explain repercussions for unmet conditions and are often nonnegotiable.

Additionally, poor financial reporting leads to penalties and failed audits. For instance, the IRS penalizes charities and nonprofits that fail to file their tax return by the due date, costing $20 per day. The same penalty applies for incomplete and incorrect tax returns, with the maximum penalty being the lesser of $10,500 or 5% of your nonprofit’s gross receipts for the year.

The Single Audit Act states that grant recipients can be subject to an audit annually to ensure compliance with government regulations. Conducting routine internal reviews, whether monthly, quarterly or during key project milestones, can ensure your spending aligns with grant conditions. Comparing actual expenditures to your budget enables proactive adjustments and prevents overspending or underutilization — underutilizing funds can also lead to clawbacks.

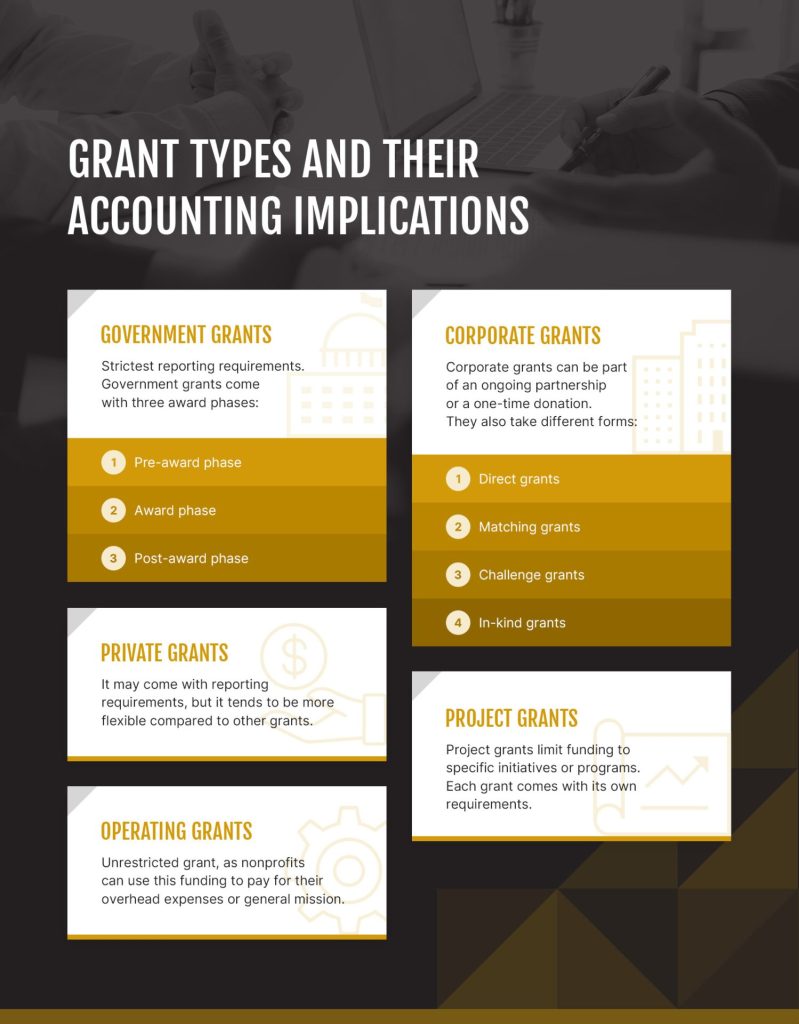

Grant Types and Their Accounting Implications

Some grants come with stricter requirements than others. Payment methods also vary, where some grants pay through reimbursements instead of paying up front. Check the grant terms so you can plan and allocate funds effectively. Grants generally fall under one of the following categories:

Government Grants

Government grants fund an organization’s ideas or projects that benefit the economy or provide public services. They often support innovative research, critical recovery initiatives and other programs listed in the annual publication of assistance listings. They’re one of the many forms of federal financial assistance. However, they also have the strictest reporting requirements.

Government grants come with three award phases:

- Pre-award phase: This phase includes the grant announcement and the application submissions and review.

- Award phase: Final award decisions come from the federal agency staff with fiduciary responsibility and legal authority to enter into agreements. They often make award recommendations based on the financial and programmatic reviews of the applications.

- Post-award phase: Once you receive an award, the federal agency assists and ensures you comply with the grant terms and conditions.

Corporate Grants

Corporate grants are provided by companies to nonprofits to support specific missions, initiatives or projects. These grants are often part of the corporate social responsibility initiatives, which also means agreements can include branding or publicity obligations. Companies often award grants based on a nonprofit’s alignment with company goals and community impact objectives.

Corporate grants can be part of an ongoing partnership or a one-time donation. They also take different forms:

- Direct grants: These grants are cash or funding that supports a specific project or program.

- Matching grants: These grants involve companies matching employee donations on a dollar-for-dollar basis.

- Challenge grants: These grants involve a company pledging to contribute funds if your nonprofit can raise a specific amount from other sources.

- In-kind grants: These noncash grants often involve product donations and services that can assist you in your projects or operations.

Getting a corporate grant can increase your nonprofit’s visibility and credibility, especially if the company is well-known and reputable. You can easily build trust with volunteers, donors and other stakeholders, as the award signals that you’re capable of managing significant funding.

To increase your chances of approval, you need to demonstrate how you’ve provided tangible results and how you plan to measure success. You also need a detailed budget showcasing how the funds can support your project’s goals. You may have to highlight how your nonprofit can sustain the project after you’ve exhausted the corporate grant.

Private Grants

A private grant is funded by foundations or individual donors. It may come with reporting requirements, but tends to be more flexible compared to other grants. Grantors are often willing to provide seed money or general operating support, so you can experiment with new ideas or invest in infrastructure.

While private grants have simpler technical requirements, they often have higher relationship gates, where grantors favor nonprofits or organizations with which they have an existing relationship. Networking is often part of an organization’s strategy to secure private grants.

Project Grants

Project grants limit funding to specific initiatives or programs. You must often track spending for these grants separately from other sources. Your spending must also align with the approved project scope and timeline. Each grant comes with its own requirements.

For instance, a project grant may require projects to be related to a specific field of study. You may also need to demonstrate that your nonprofit has the qualities to complete the project.

Operating Grants

An operating grant is also known as an unrestricted grant, as nonprofits can use this funding to pay for their overhead expenses or general mission. For instance, you can use it for rent, salaries and daily operational expenses. It may have broader conditions than other grants, but still requires careful financial reporting. Because these grants often come from individual donors, there’s typically no standard application process.

Operating grants are popular, making the application process competitive and rigorous. Presenting an impeccable track record and demonstrating your trustworthiness through accurate financial reports can increase your chances of approval.

How to Ensure Accurate Financial Reporting

Accurate financial reporting is feasible by adopting certain strategies:

- Maintain a centralized documentation system: Having a dedicated location for your financial documents makes it easier to access the right information quickly. This centralization mitigates the risk for human error and helps you avoid missing reporting and filing deadlines.

- Review and reconcile accounts regularly: Many accounting teams reconcile accounts with long gaps in between sessions or too closely to relevant deadlines. Creating a consistent workflow for account reconciliations improves accuracy and expedites account reviews.

- Use effective accounting and management tools: Many resources are available to help nonprofits improve financial reporting practices. For instance, a spreadsheet can help you maintain accurate financial records, while budget trackers can help you generate relevant reports. Automation provided by these tools can help you meet grantor deadlines.

- Leverage accounting services: You don’t always need in-house expertise, which adds to your overhead expenses. Working with professional accounting services can be more cost-effective given their experience, saving you time and resources. These services also help you stay on top of relevant regulations, increasing your chances of securing future grants.

Frequently Asked Questions

Nonprofits commonly ask the following questions to further understand grant fund management:

What Is Grant Accounting?

Grant accounting, also known as grant management accounting, involves tracking how your organization uses the grant funds to make sure you comply with the agreement. Accurate grant accounting enables you to use funds wisely and sustainably, so you can avoid negative repercussions while ensuring that every dollar makes a difference.

What Is the Difference Between Fund and Grant Accounting?

Fund accounting is the overhead framework, where grant accounting is its subset. Similarly, fund accounting tracks a nonprofit’s financial activities, but instead of focusing on grants, it includes tracking activity across funding sources. For instance, these sources may include individual donations, membership fees and charity crowdfunding. Grant accounting helps ensure you’re spending grant funds according to the terms.

What Do Grant Accountants Do?

Grant accountants manage your grant funds. Their duties often involve:

- Tracking grant expenses.

- Ensuring compliance with relevant regulations and grant terms.

- Preparing financial reports.

- Supporting audits and grantor reviews.

Accurate Financial Reporting Strengthens Trust With Grantors

Accurate financial reporting helps you secure grants, as it demonstrates your nonprofit’s reliability and trustworthiness. It’s often a requirement of grantors, especially for government grants with strict regulations. Without accurate reporting, you risk fund misuse, overspending, clawbacks and even fraud charges.

To increase your chances of securing grants, review the grantor’s requirements thoroughly. Financial reporting requirements may also come with performance requirements that showcase the fund’s tangible impact. Having a centralized system and leveraging accounting tools can help with accurate documentation. You can also work with professional accounting services to make the process easier.